Small and medium-sized enterprises are the backbone of the economy. Katharine Freeland looks at the snowballing challenges facing legal advisers who are helping these businesses to scale up or sell up

The low down

Small and medium-sized enterprises (SMEs) should be front and centre of the industrial and wealth strategies of any incoming government. The ease and confidence with which these businesses can merge, acquire or be acquired is of huge importance. In such deals, a small business lawyer may find an elite City firm on the other side, especially in the technology sector, where big players buy innovative businesses for ‘first mover’ advantage. Globally, private equity funds are targeting SMEs, correctly identifying the potential for targets to grow. But how to price and undertake due diligence on potential is an increasingly complex challenge for corporate lawyers, who must consider factors ranging from national security to artificial intelligence. The SME sector is also new to the transparency demands of ESG reporting.

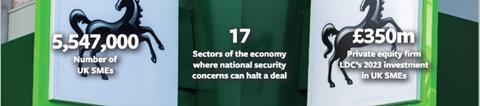

The state of a country’s SME sector is a measure of its economic vigour. These businesses are engine rooms that create jobs and present valuable opportunities for entrepreneurship and innovation. Government statistics show that as of October 2023, there were 5.6 million businesses in the UK, 5,547,000 of which qualify as small (0-49 employees) or medium-sized (50-249), meaning that 99.05% of UK businesses are SMEs. Cultivating an SME client base provides lawyers with the opportunity to build meaningful and lasting relationships.

Richard Cobb, head of corporate at south-west firm Michelmores, says: ‘It is satisfying as a lawyer to steer a founder or management team from small startup through the scaling-up process – through various acquisitions, divestments, carve-outs – to the eventual exit, whether this is a sale or a stock market listing.’

Tech M&A predominates

The emphasis on digital transformation in the workplace means that technology sector M&A is a particular focus. Whatever the industry, there is a tech function promising next-level improvement: agritech, fintech, medtech, insurtech, cleantech (products, processes or services designed to reduce negative environmental impacts) and deeptech (multidisciplinary tech innovations aimed at solving global challenges such as climate change).

Instead of building their own tech capabilities, acquirers can quickly gain access to proprietary technology that allows them ‘first mover’ advantage. By focusing on such vertical integration, acquirers not only elevate their own tech but lower costs and simplify business practice by gaining control over the supply chain.

An example of a successful insurtech deal was RVU’s acquisition of Tempcover, an online platform that provides temporary insurance solutions, from specialist private client alternative investor Connection Capital. Freshfields advised RVU, the owner of Confused.com, USwitch.com and Money.co.uk; commercial firm Gateley advised Connection Capital, having steered Tempcover throughout its investment cycle from MBO to follow-on investment and finally to its exit.

Deeper due diligence required

With the artificial intelligence (AI) revolution, businesses that focus on AI, machine learning, deep learning and the ‘internet of things’ are in demand, particularly in sectors such as healthcare. Technology that uses data mining, image processing and predictive modelling to generate actionable insights is gold dust to potential business partners such as pharma companies.

Yet the faster technology evolves, the more uncertainty is introduced into the deal process. For example, putting a value on a business with seemingly limitless potential is difficult, and there are often differences of opinion. The rise in earn-out deals – contractual provisions allowing the seller of the business to obtain additional compensation if that business achieves certain financial goals – is a consequence of this uncertainty. Earn-out provisions are becoming increasingly complex and creatively structured, reaching beyond measuring return on investment.

The pace of technological change has also created a need for deeper – and more intrusive – due diligence. Lawyers must understand the precise function of the tech in question to determine whether a notification is required under the National Security and Investment Act 2021. Sometimes an independent expert is enlisted to analyse a target’s products and services before the deal can progress.

‘Technology businesses are becoming so advanced that lawyers, who are not industry experts, can sometimes reach the limits of their cognitive abilities in understanding them,’ says Kingsley Napley’s Glafkos Tombolis, who regularly advises on healthcare data M&A transactions, and corporate and business owners operating in the cybersecurity, enterprise software, retail and digital marketing sectors. ‘But it is crucial to work out exactly what the target does to assess whether it falls within the ambit of the act.’

Before the National Security and Investment Act came into force in 2021, the ability of the government to intervene in transactions was circumscribed and only possible through limited provisions in the Enterprise Act 2002.

Now, if the deal falls within 17 specified management sectors and the buyer does not make a mandatory notification when required, a criminal offence is committed and the business can incur heavy fines, as well as having the deal voided. There is no materiality threshold, and the act covers investments as well as acquisition of control.

Tombolis says: ‘The act affects the deal timetable in needing to build in time to notify, wait, receive a government review, then possibly mitigate and provide remedies. It is a draconian and very consequential piece of legislation – with the power to completely wreck transactions and make the business case for the deal less certain.’

Extended due diligence is not just a feature of tech deals. ‘There are more complexities in M&A deals relating to financial arrangements and the range of capital solutions used,’ says Nigel Taylor, corporate and M&A partner at London firm Wedlake Bell. ‘Deals are taking longer, as the parties are not just kicking the tyres but lifting the bonnet.’

National Security and due diligence

The National Security and Investment (NSI) Act 2021 hands the government significant powers to intervene in transactions. It is not explicitly modelled on the Committee for Foreign Investment in the United States (CFIUS), an interagency committee chaired by the Secretary of the Treasury, but the act does reflect a global trend towards a more interventionist approach to national security. CFIUS was beefed up in 2018 by the Foreign Investment Risk Review Modernization Act, enhancing its authority to review foreign investments in US businesses, and it continues to be regularly tightened. In the European Union, meanwhile, the EU’s Foreign Direct Investment Regulation came into force in each member state in 2020.

The NSI act significantly expands the types of transaction covered by national security reviews. Along with mergers and acquisitions, minority investments, acquisition of voting rights and acquisitions of assets all potentially fall under its scope if they reach trigger thresholds. The lowest percentage threshold triggering a mandatory notification under the act requires an acquisition of more than 25% of voting rights or shares in a qualifying entity – which can be domestic or foreign.

Seventeen sensitive economy sectors are listed. If dealing with a business that operates in – or is closely linked to – these sectors, it is wise to consider whether this triggers a mandatory notification. There is also a voluntary notification system for transactions that do not fall into the mandatory notification definition but may pose national security concerns. The 17 sectors are: advanced materials, advanced robotics, artificial intelligence, civil nuclear, communications, computing hardware, critical suppliers to government, cryptographic authentication, data infrastructure, defence, energy, military and dual-use, quantum technologies, satellite and space technologies, suppliers to the emergency services, synthetic biology, and transport.

National security is not defined in the act, allowing the government broad scope for intervention and flexibility to capture evolving risks. Failure to comply has serious consequences. These include criminal liability (imprisonment for up to five years) and hefty fines which can constitute the greater of 5% of worldwide turnover or £10m. The transaction can also be voided if it falls under a mandatory obligation to report.

Time spent evaluating whether the deal falls under the act should be accounted for in deal timelines. Client expectations must also be managed to avoid delay or the prospect of government intervention.

Environmental, social and governance

The rise in EU ESG-related regulation, together with the reputational risk of unfulfilled or misleading sustainability commitments, mean that deeper due diligence probes are more important than ever (see ‘Seeing and believing’, Gazette, 14 June).

An acquirer should examine a target’s ESG policies and procedures to check they are robust, as well as analysing their sanctions and exports controls and cybersecurity. Where there are complex supply chains in play, there is a potential risk of governance breaches, corruption, bribery and fraud. All these factors are under more scrutiny from warranty and indemnity insurers, with an impact on negotiation over the scope of warranties drafted.

The Economic Crime and Corporate Transparency Act 2023 is also relevant here. Acquirers will not want to end up in the line of fire for the new ‘failure to prevent’ offence for fraud, expected to come into force in early 2025. The act also contains changes to the identification principle required for prosecution. Rather than identifying the individual who is the ‘directing mind and will’ of the entity, it is now sufficient to identify a responsible ‘senior manager’. This poses an extra layer of risk for the acquirer.

‘Technological innovation and its interface with national security, together with ESG considerations, are gumming up the deal process and making them more protracted and complex, with a growing need to draft thorough walkaway rights,’ says Tombolis.

But ESG presents an opportunity as well as a risk. Strong ESG credentials in a business are increasingly desirable. They are perceived as a sign of a positive working culture, high staff retention, and commitment to brand and reputation.

Sales to staff, where employees hold significant ownership in the business through employee share ownership plans, worker cooperatives or mutuals, are also increasing. Tombolis notes: ‘Employee ownership trusts can be a useful tool for democratising the business and improving ESG credentials. They are also tax efficient because the sale does not crystallise CGT.’

ESG knowledge and reporting are becoming essential across every business sector up and down the supply chain. Thus, businesses that specialise in ESG and sustainability have become valuable acquisition targets. One example is London-based sustainability advisory and solutions firm Anthesis, in which private equity investor Carlyle Capital is a majority shareholder. Anthesis has made six ESG acquisitions in the past 18 months. The latest was ‘purpose-driven’ marketing company Revolt, which supports the C-suite with projects across sustainability, DEI strategy and communications.

Private equity

In December 2023 S&P Global estimated that private equity was sitting on around $2.6 trillion of capital ready for deployment. Driven by the need to create deal flow and produce returns for limited partners, private equity has turned to SMEs, which have the advantage of agility, the potential to grow quickly, and, as lower-value businesses, can be purchased without large levels of debt – crucial at a time of higher interest rates.

UK-based private equity investor LDC, the private equity arm of Lloyds Banking Group, is a case in point. Investing £350m into UK-based SMEs in 2023, LDC announced that it was planning to grow that figure in 2024. Last year LDC invested £300m in 14 new businesses and provided £50m of follow-on funding to its existing portfolio of more than 90 companies, as well as supporting 46 bolt-on acquisitions. New investments included sustainability data and technology provider Sedex, specialist product agency Star Live, AI-based talent analytics platform Horsefly and managed service provider DSP.

Buying bolt-ons is essential to the ‘buy-to-build’ strategies currently used by private equity investors to deliver growth. In this scenario a platform company is used to make around four or more sequential add-on acquisitions of smaller companies, with SaaS (software as a service) additions proving particularly popular. The SME market is the place to find these opportunities.

Cashing in

Having battled adverse conditions over the past few years, it is no surprise that some owner-managers want out. Sellers invest considerable time and resources in exit strategies, including implementing robust company policies and procedures, reviewing tax positioning, and creating effective succession planning.

Currently, there is an appetite among international acquirers scoping out the UK SME market. ‘EU companies which have found it difficult to access UK markets after Brexit are seeking acquisitions,’ says Tombolis. ‘There is also considerable interest from US buyers, given the strength of the dollar against the pound.’ It remains to be seen whether there will be a flurry of UK deals with a US nexus closing before the US election in November. With more than 40 elections scheduled around the world in 2024, political upheaval can substantially affect deal flow, depending on the business sector and jurisdictions covered.

Looking ahead

The looming UK general election has had an impact on SMEs. Some are keen, their advisers report, to get deals over the line before an expected Labour victory. Others at formative deal stages prefer to wait and see. Lawyers report that SME clients are apprehensive about possible changes in tax policies or regulations that may affect deal terms.

Labour stated in March that it has no plans to increase capital gains tax. It also ruled out rises to income tax, national insurance and corporation tax. A concern for SMEs is that, even in the event of no direct tax rises, reliefs (such as on business asset disposal) will be removed. Any changes to taxes or reliefs are likely to cause a rush of activity in the SME M&A market, akin to when the lifetime limit on entrepreneurs relief was lowered from £10m to £1m in 2020.

AI legislation could also affect deals. The last government’s AI white paper, published in March, set out its ‘pro-innovation’ approach. This contrasts with the EU’s plan to introduce a stricter statutory framework under its proposed Artificial Intelligence Act. If the differing approaches to AI regulation across jurisdictions come to pass, there are likely to be further due diligence challenges on cross-border M&A deals which may extend timeframes. More teamwork between lawyers, owner-managers, management teams and tech-sector specialists may be necessary to push an AI-focused M&A deal over the line.

All this comes against adverse headwinds in global markets, more distressed deals, reorganisations and likely carve-outs. The attraction of AI and its adjacent technologies will only grow, while the ongoing reduction in the numbers of skilled workers – crucial to the operation of many businesses in the SME sector – may lead to SMEs that offer the potential to achieve operational efficiencies through AI being the most highly prized targets.

Katharine Freeland is a freelance journalist

No comments yet